Build-To-Rent

PROPERTY STRATEGY

Explore the possibilities and discover the potential of Build-To-Rent (BTR) as a Buy-To-Let Strategy.

New to Build-To-Rent?

Learn the basics of Build-To-Rent (BTR) as a buy-to-let investment strategy through our introductory video.

Below, we have provided more detailed information about Build-To-Rent as a strategy for Buy-To-Let properties.

A Definition

What is

Build-To-Rent?

Build to Rent is a sector within the property market where the accommodation is intended to be rented out to tenants by the owner instead of being occupied.

To meet the growing demands for city centre housing, Build-To-Rent is a popular sector for house builders and property developers.

Property Types

Build-To-Rent covers all properties that are built to be rented rather than owner-occupied so this can cover a broad range of properties. Currently most are being built as leasehold apartments within a block as it allows developers to produce more housing in a smaller area. However, a growing number of single-family homes are being built as Build-To-Rent to meet the growing demands of tenants who need rental accommodation with more space and in more rural and semi-rural locations.

Let's take a look at some of the advantages and disadvantages of Build-To-Rent

One of the main attractions of BTR as a buy-to-let property strategy is the discount offered on the open market price, Developers want to secure sales while the property is being built so that by the time of completion the development is sold out. To make this attractive to buyers they offer a discount on the price the apartments would sell for when the development is complete.

While lending can be limited for other strategies, with BTR there are usually lots of lenders available, depending on the construction type of the building.

New build properties have to be covered by a structural warranty on completion, one of the most common is the NHBC 10-year warranty.

There are many BTR developments across towns and cities in the UK which means you are not likely to be limited in your choice of location which can be the case with other more restricted strategies.

With BTR properties in high demand from tenants, the large pool of lending options and the lower price point it is a popular strategy giving an easier exit strategy.

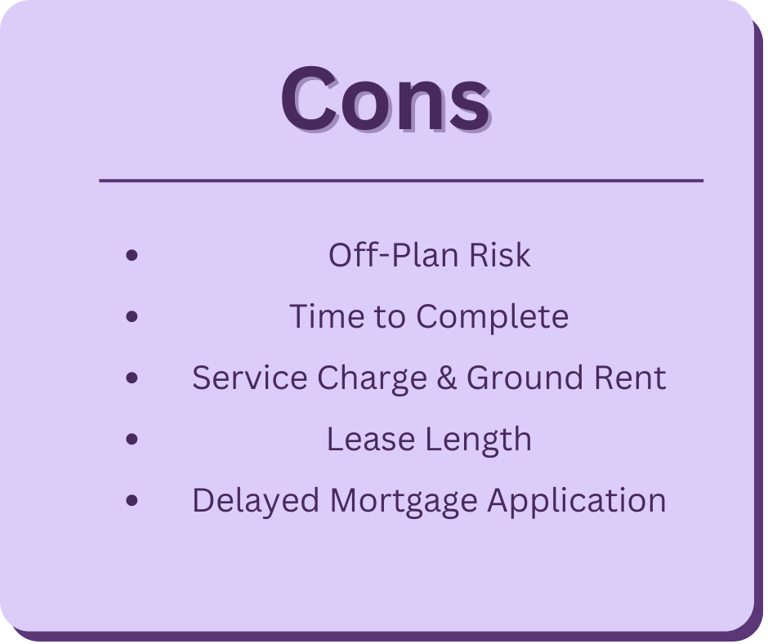

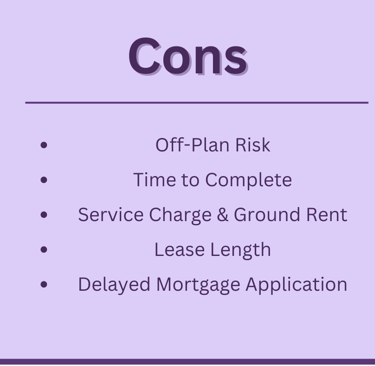

Although there are numerous benefits to owning BTR property, there are also some downsides to this strategy.

The main risk that is associated with BTR properties is that they are still under construction and this means that there is always a risk to the property not being completed on schedule or to the specification that was first anticipated when the construction started.

As a lot of BTRs are leasehold apartments there is a service charge payable to the block manager, depending on the time of completion there also may be ground rent payable to the freeholder who owns the building containing the apartments. These additional costs reduce the overall take-home returns from the property.

In addition to the properties being leasehold, the lease length is set by the developer when sold. If the lease length is considered short for leasehold property then it can restrict the number of lending options available and can make re-sale of the property more difficult.

BTRs that are sold off plan are purchased in a different way to properties that are already built, one aspect of this is the mortgage application, these are carried out close to completion of the project. As this could be up to 2 years from when you commit to the purchase the mortgage market can change, and this could affect the lending options available to the buyer at the point of completion.

How much do I need for a BTR?

Cash Requirement

The cash requirement for BTR can often be one of the lowest in the buy-to-let market. With properties being available in a number of locations and ranging in price within a development it makes them more accessible than other strategies.

Depending on the prices in the local area, a starting budget of around £50,000 could be sufficient to purchase a leasehold BTR apartment if using a mortgage. As financing would typically be available for the property purchase, the price for the property could be up to £160,000 but you would need to cover the deposit and any purchasing costs so this may vary.

Off Plan or Completed Purchase

We've scored this one a 1 out of 5 difficulty, it is one of the easiest buy-to-let strategy types and a great option for someone new to property.

There are often several Build-To-Rent projects available within most towns and cities, containing a large number of units which means there is a wide range of opportunities.

Once you've acquired a suitable property, the management of the tenancy can be fairly straightforward if you are using a standard assured shorthold tenancy (AST) and there will be a high tenant demand in larger city centres.

Level of Difficulty

How much work is involved with BTR?

Owner Involvement

When the purchasing element is removed from the equation and you focus on the ongoing ownership, BTR has a low level of involvement from the owner, and it can be minimal if you employ a letting agent to manage the property and find new tenants when required.

Because this type of property can be let to any tenants you approve it is often easier to find someone to occupy the property. You will need to manage any repairs or maintenance for the property, although with new BTR properties, they benefit from a 10-year warranty so this should be minimal over the first decade following completion. Again if you employ a letting agent to manage the property this can be further reduced as they will often arrange these works and simply request authorisation from the owner.

Typical Returns & Timeframes

What should you expect from BTR?

Exit Strategy

What happens if you want to sell and how easy is it to liquidate your cash?

Just like many other property investment strategies, you can sell a BTR property if there is an existing tenancy agreement in place, it will typically be transferred to the new owner upon completion of the sale. The new owner will then start receiving rental payments directly from the tenants.

BTR properties have an easy exit strategy as they can appeal to owner-occupiers looking for a residential home or another buyer looking for a buy-to-let property. Coupled with the fact that the properties can often be purchased using a mortgage it further opens up the list of potential buyers.

Because of the wide range of potential buyers, selling via a high street estate agent is typical and you would not necessarily need to enlist the help of specialist property sales agents, like you may need to with other specialised strategies.

Registered Company Number: 15439671

Copyright © 2025 Seven Generations UK Limited, All Rights Reserved

PRS Membership Number: PRS043981

Your trusted partner for UK buy-to-let property

Quick Links

Contact Us

ICO Membership Number: ZB694046

Properties For Sale